Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Holiday Gifts Are Not the Only Hot Things Right Now

Black Friday is behind us and holiday gifts are flying off the shelves in stores and online. Unlike last year, however, there’s another type of buyer that is very active this winter – the homebuyer.

Each month, ShowingTime releases their Showing Index, which tracks the average number of appointments received on active U.S. house listings. The latest index revealed:

“Traffic was more active once again compared to 2018, as the nation saw its third straight month of higher year-over-year showing activity…The 5.5% increase in showings nationwide was the largest jump in activity during the now three-month streak of year-over-year increases vs. 2018.”

The same report indicates showings increased in every region of the country:

- The South increased by 10.8%

- The West increased by 8.6%

- The Northeast increased by 3.8%

- The Midwest increased by 1.5%

Why is the traffic more active?

One of the main reasons buyer traffic has increased year-over-year is that mortgage rates have fallen dramatically. According to Freddie Mac, the average mortgage rate last December was 4.64%. Today, the rate is almost a full percentage point lower!

Bottom Line

There are first-time, move-up, and move-down buyers actively looking for the home of their dreams this winter. If you’re thinking of selling your house in 2020, you don’t need to wait until the spring to do it. Your potential buyer may be searching for a home in your neighborhood right now.

A 365 Day Difference in Homeownership

Over the past year, mortgage rates have fallen more than a full percentage point. This is a great driver for homeownership, as today’s low rates provide consumers with some significant benefits. Here’s a look at three of them:

- Refinance: If you already own a home, you may want to decide if you’re going to refinance. It’s one way to lock in a lower monthly payment and save substantially over time, but it also means paying upfront closing costs too. You have to answer the question: Should I refinance my home?

- Move-up or Downsize: Another option is to consider moving into a new home, putting the equity you’ve likely gained in your current house toward a down payment on a new one that better meets your needs – something that’s truly a perfect fit for your family.

- Become a First-Time Homebuyer: There are many financial and non-financial benefits to owning a home, and the most important thing is to first decide when the time is right for you. You have to determine that on your own, but know that now is a great time to buy if you’re considering it. Just take a look at the cost of renting vs. buying

Why 2019 Was a Great Year for Homeownership

Last year at this time, mortgage rates were 4.63% (substantially higher than they are today). If you’re one who waited for a better time to make a move, market conditions have improved significantly. Today’s low mortgage rates combined with increasing wages are making homes much more affordable than they were just one year ago, so it’s a great time to get more for your money and consider a new home.

The chart below shows how much you would save based on today’s rates, compared to what you would have paid if you purchased a house exactly one year ago, depending on how much you finance.

Bottom Line

If you’ve been waiting since last year to make your move into homeownership or to find a house that better meets your needs, today’s low mortgage rates may be just what you need to get the process going. Let’s get together to discuss how you can benefit from the current rates.

Have You Budgeted for Closing Costs?

Saving for a down payment is a key step in the homebuying process, and it’s not the only piece you need to include in your budget. Another factor that’s important to plan for is the closing costs required to obtain a mortgage.

What Are Closing Costs?

According to Trulia,

“When you close on a home, a number of fees are due. They typically range from 2% to 5% of the total cost of the home, and can include title insurance, origination fees, underwriting fees, document preparation fees, and more.”

For those who buy a $250,000 home, for example, that amount could be between $5,000 and $12,500 in closing fees. Keep in mind, if you’re in the market for a home above this price range, your costs could be significantly greater. As mentioned before,

Closing costs are typically between 2% and 5% of your purchase price.

Trulia gives more great advice, saying,

“There will be lots of paperwork in front of you on closing day, and not enough time to read them all. Work closely with your real estate agent, lender, and attorney, if you have one, to get all the documents you need ahead of time.

The most important thing to read is the closing disclosure, which shows your loan terms, final closing costs, and any outstanding fees. You’ll get this form about three days before closing since, once you (the borrower) sign it, there’s a three-day waiting period before you can sign the mortgage loan docs. If you have any questions about the numbers or what any of the mortgage terms mean, this is the time to ask—your real estate agent is a great resource for getting you all the answers you need.”

Bottom Line

Let’s get together to discuss the home buying process, to be sure your plan includes budgeting for what you need to purchase your dream home – without any surprises!

Millennials Are on the Move as First-Time Homebuyers [INFOGRAPHIC]

![Is Your First Home Now Within Your Grasp? [INFOGRAPHIC] | MyKCM](https://desireestanley.com/files/2019/12/20191206-MEM-1046x1477.jpg)

![Is Your First Home Now Within Your Grasp? [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2019/12/05064901/20191206-MEM-1046x1477.jpg)

Some Highlights:

- According to NAR’s latest Profile of Home Buyers & Sellers, the median age of all first-time homebuyers is 32.

- With more millennials entering a homebuying phase of life, they are driving a large portion of the buyer’s appetite in the market, keeping buyer activity strong.

- More and more “old millennials” (ages 25-36) are realizing that homeownership is now within their grasp, and they’re actively dominating the first-time homebuyer market!

It’s ‘National Roof Over Your Head’ Day!

Did you know that each year in the United States, we celebrate “National Roof Over Your Head Day” on December 3rd?

As noted on the National Calendar, it was “created as a day to be thankful for what you have, starting with the roof over your head. There are many things that we have that we take for granted and do not stop to appreciate how fortunate we are for having them.”

From bungalows to cottages, and farmhouses to treehouses, today we show our appreciation and gratitude for the places we call home. Owning the roof that shelters us is something many renters still aspire to, knowing there are so many financial and non-financial benefits to homeownership.

According to the 2019 State of the Nation’s Housing from the Joint Center for Housing Studies of Harvard University,

“Cost-burdened renters now outnumber cost-burdened homeowners by more than 3.0 million. In addition, renters make up 10.8 million of the 18.2 million severely burdened households that pay more than half their incomes for housing.”

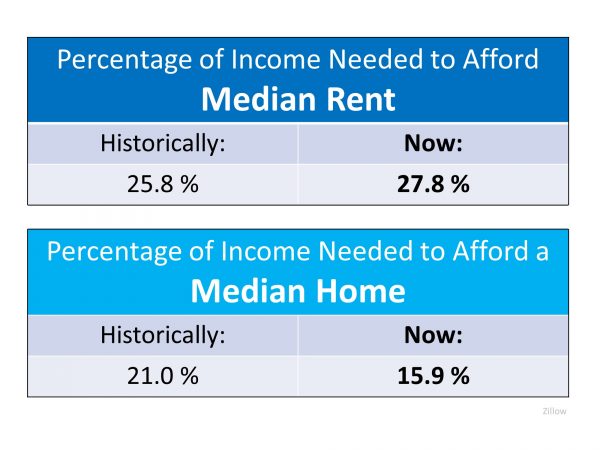

Homeownership drives many benefits, including providing families with a place to feel secure. It also helps promote confidence that they are investing proactively in themselves and their communities. That is why there are 77.7 million owner-occupied housing units in the United States.

Many, however, fear it is too expensive to own a home. In reality, however, it’s actually more expensive to rent. Here’s the breakdown as a percentage of income necessary for both – affording median rent and owning a home:

Bottom Line

Today we pause to appreciate the places we call home, and all of the other reasons we have to be truly thankful. For those who don’t own yet and would like to, it’s a wonderful time to start identifying the steps to take toward homeownership. Let’s connect today to begin creating your plan.

7 Reasons to List Your House This Holiday Season

Around this time each year, many homeowners decide to wait until after the holidays to list their houses. Similarly, others who already have their homes on the market remove their listings until the spring. Let’s unpack the top reasons why listing your house now or keeping it on the market this winter may be the best choice you can make.

Here are seven great reasons not to wait:

- Relocation buyers are out there now. Many companies are still hiring throughout the holidays, and they need their new employees to start as soon as possible.

- Purchasers who are looking for homes during the holidays are serious buyers and are ready to buy now.

- You can restrict the showings on your home to days and times that are most convenient for you. You will remain in control.

- Homes show better when decorated for the holidays.

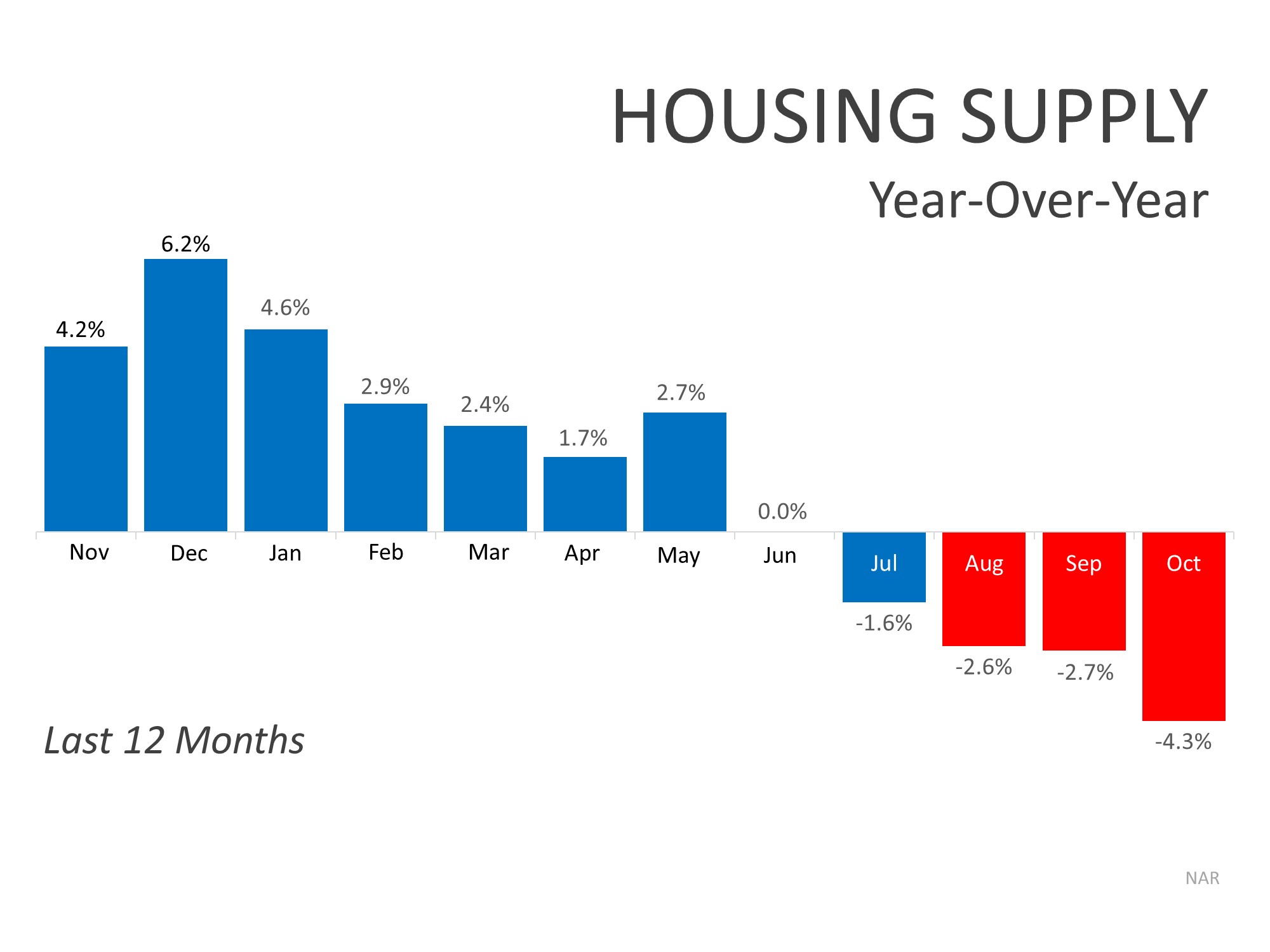

- There is minimal competition for you as a seller right now. Over the past few months we’ve seen the supply of homes for sale decreasing year-over-year, as shown in the graph below:

- The desire to own a home doesn’t stop during the holidays. Buyers who were unable to find their dream homes during the busy spring and summer months are still searching, and your home may be the answer.

- Late fall and early winter make up the “sweet spot” for sellers. The supply of listings increases substantially after the holidays. Also, in many parts of the country, new construction will continue to surge and reach new heights in 2020, which will lessen the demand for your house next year.

Bottom Line

It may make the most sense to list your home this holiday season. Let’s get together to determine if selling now is your best move.

How Long Can This Economic Recovery Last?

The economy is currently experiencing the longest recovery in our nation’s history. The stock market has hit record highs, while unemployment rates are at record lows. Home price appreciation is beginning to reaccelerate. This begs the question: How long can this economic recovery last?

The Wall Street Journal (WSJ) Survey of Economists recently called for an economic slowdown (recession) in the near future. The most recent survey, however, now shows the economists are pushing that timetable back. When asked when they expect a recession to start, 42.5% of the economists in the previous survey projected between now and the end of 2020. The most recent survey showed that percentage drop to 34.2%. Here are the most current results: Like the economists surveyed by the WSJ, most experts are still predicting a recession will likely occur sometime in the next few years. However, many are pushing back the date for the economic slowdown.

Like the economists surveyed by the WSJ, most experts are still predicting a recession will likely occur sometime in the next few years. However, many are pushing back the date for the economic slowdown.

Bottom Line

Real estate is impacted by the economy (and the consumer’s belief in the strength of the economy). The fact that most economic experts are calling for the recovery to continue through 2020 means the housing market will also remain strong for the foreseeable future.

2 Myths Holding Back Home Buyers

In a recent article, First American shared how millennials are not really any different from previous generations when it comes to the goal of homeownership; it is still a huge part of their American Dream. The piece, however, also reveals,

“Saving for a down payment is one of the biggest obstacles faced by first-time home buyers. Dispelling the 20 percent down payment myth could open the path to homeownership for many more.”

Myth #1: “I Need a 20% Down Payment”

Buyers often overestimate how much they need to qualify for a home loan. According to the same article:

“Americans still overestimate the qualifications needed to get a mortgage, resulting in qualified potential buyers not even considering homeownership. Indeed, the Urban Institute report revealed that 16 percent of consumers believed that the minimum down payment required by lenders is 20 percent or more, and another 40 percent didn’t know at all.”

While many potential buyers still think they need to put at least 20% down for the home of their dreams, they often don’t realize how many assistance programs are available with as little as 3% down. With a little research, many renters may actually be able to enter the housing market sooner than they ever imagined.

Myth #2: “I Need a 780 FICO® Score or Higher”

In addition to down payments, buyers are also often confused about the FICO® score it takes to qualify for a mortgage, believing a ‘good’ credit score is 780 or higher.

To debunk this myth, let’s take a look at Ellie Mae’s latest Origination Insight Report, which focuses on recently closed (approved) loans. As indicated in the chart above, 50.23% of approved mortgages had a credit score of 500-749.

As indicated in the chart above, 50.23% of approved mortgages had a credit score of 500-749.

Bottom Line

Whether buying your first home or moving up to your dream home, knowing your options will make the mortgage process easier. Believe it or not – your dream home may already be within your reach.

Planning on Buying a Home? Be Sure You Know Your Options.

When you’re ready to buy, you’ll need to determine if you prefer the charm of an existing home or the look and feel of a newer build. With limited existing home inventory available today, especially in the starter and middle-level markets, many buyers are considering a new home that’s recently been constructed, or they’re building the home of their dreams.

According to Robert Dietz, Chief Economist at the National Association of Home Builders (NAHB),

“The second half of 2019 has seen steady gains in single-family construction, and this is mirrored by the gradual uptick in builder sentiment over the past few months.”

This is great news for homebuyers because it means there is additional inventory coming to the market, giving buyers more choices. The most recent data from NAHB shows,

“The inventory of new homes for sale was 321,000 in September, representing a 5.5 months’ supply. The median sales price was $299,400. The median price of a new home sale a year earlier was $328,300.”

Another added bonus is that builders are very aware of buyer demand in this segment, so they’re now building in a price range where there are more interested buyers ($299,400 instead of $328,300). With a reduced sales price and low-interest rates, today’s buyers have strong purchasing power.

Bottom Line

If you’re thinking of buying a home, you may want to consider a new build to meet your family’s needs. Let’s get together to discuss the process and review what’s available in our area.

4 Reasons to Buy a Home This Fall

Here are four great reasons to consider buying a home today, instead of waiting.

1. Prices Will Continue to Rise

CoreLogic’s latest Home Price Insights Report shows that home prices have appreciated by 3.6% over the last 12 months. The same report predicts prices will continue to increase at a rate of 5.8% over the next year.

The bottom in home prices has come and gone. Home values will continue to appreciate for years. Waiting no longer makes sense.

2. Mortgage Interest Rates Are Projected to Increase Next Year

The Primary Mortgage Market Survey from Freddie Mac indicates that interest rates for a 30-year mortgage have recently hovered just above 3.5%. This is great news for buyers in the market right now, because low-interest rates increase your purchasing power – but don’t wait! Most experts predict rates will rise over the next 12 months. The Mortgage Bankers Association, Fannie Mae, Freddie Mac, and the National Association of Realtors are in unison, projecting that rates will increase by this time next year.

An increase in rates will impact your monthly mortgage payment. A year from now, your housing expense will increase if a mortgage is needed to buy your next home.

3. Either Way, You Are Paying a Mortgage

There are some renters who haven’t purchased a home yet because they’re uncomfortable taking on the obligation of a mortgage. Everyone should realize that, unless you’re living rent-free with your parents, you are paying a mortgage – either yours or that of your landlord.

As an owner, your mortgage payment is a form of ‘forced savings’ that allows you to have equity in your home you can tap into later in life. As a renter, you guarantee your landlord is the person with that equity.

Are you ready to put your housing costs to work for you?

4. It’s Time to Move on With Your Life

The ‘cost’ of a home is determined by two major components: the price of the home and the current mortgage rate. It appears both are on the rise.

But what if they weren’t? Would you wait?

Look at the actual reason you’re buying and decide if it is worth waiting. Whether you want to have a great place for your children to grow up, you want your family to be safer, or you just want to have control over custom renovations, maybe now is the time to buy.

Bottom Line

Buying a home sooner rather than later could lead to substantial savings. Let’s get together to determine if homeownership is the right choice for you and your family this fall.