Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Buying a Home: Do You Know the Lingo? [INFOGRAPHIC]

![Buying a Home: Do You Know the Lingo? [INFOGRAPHIC] | MyKCM](https://desireestanley.com/files/2020/03/20200313-MEM-EN-1046x1308.jpg)

![Buying a Home: Do You Know the Lingo? [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2020/03/09122748/20200313-MEM-EN-1046x1308.jpg)

Highlights:

- Buying a home can be intimidating if you’re not familiar with the terms used throughout the process.

- To point you in the right direction, here’s a list of some of the most common language you’ll hear along the way.

- The best way to ensure your home buying process is a positive one is to find a real estate professional who will guide you through every aspect of the transaction with ‘the heart of a teacher.’

Two Big Myths in the Home buying Process

The 2020 Millennial Home Buyer Report shows how this generation is not really any different from previous ones when it comes to homeownership goals:

“The majority of millennials not only want to own a home, but 84% of millennials in 2019 considered it a major part of the American Dream.”

Unfortunately, the myths surrounding the barriers to homeownership – especially those related to down payments and FICO® scores – might be keeping many buyers out of the arena. The piece also reveals:

“Millennials have to navigate a lot of obstacles to be able to own a home. According to our 2020 survey, saving for a down payment is the biggest barrier for 50% of millennials.”

Millennial or not, unpacking two of the biggest myths that may be standing in the way of homeownership among all generations is a great place to start the debunking process.

Myth #1: “I Need a 20% Down Payment”

Many buyers often overestimate what they need to qualify for a home loan. According to the same article:

“A down payment of 20% for a home of that price [$210,000] would be about $42,000; only about 30% of the millennials in our survey have enough in savings to cover that, not to mention the additional closing costs.”

While many potential buyers still think they need to put at least 20% down for the home of their dreams, they often don’t realize how many assistance programs are available with as little as 3% down. With a bit of research, many renters may be able to enter the housing market sooner than they ever imagined.

Myth #2: “I Need a 780 FICO® Score or Higher”

In addition to down payments, buyers are also often confused about the FICO® score it takes to qualify for a mortgage, believing they need a credit score of 780 or higher.

Ellie Mae’s latest Origination Insight Report, which focuses on recently closed (approved) loans, shows the truth is, over 50% of approved loans were granted with a FICO® score below 750 (see graph below): Even today, many of the myths of the home buying process are unfortunately keeping plenty of motivated buyers on the sidelines. In reality, it really doesn’t have to be that way.

Even today, many of the myths of the home buying process are unfortunately keeping plenty of motivated buyers on the sidelines. In reality, it really doesn’t have to be that way.

Bottom Line

If you’re thinking of buying a home, you may have more options than you think. Let’s connect to answer your questions and help you determine your next steps.

10 Steps to Buying a Home [INFOGRAPHIC]

![10 Steps to Buying a Home [INFOGRAPHIC] | MyKCM](https://desireestanley.com/files/2020/03/20200228-MEM-EN-1046x837.jpg)

![10 Steps to Buying a Home [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2020/02/25113646/20200228-MEM-EN-1046x837.jpg)

Some Highlights:

- If you’re thinking of buying a home and you’re not sure where to start, you’re not alone.

- Here’s a guide with 10 simple steps to follow in the homebuying process.

- Be sure to work with a trusted real estate professional to find out the specifics of what to do in your local area.

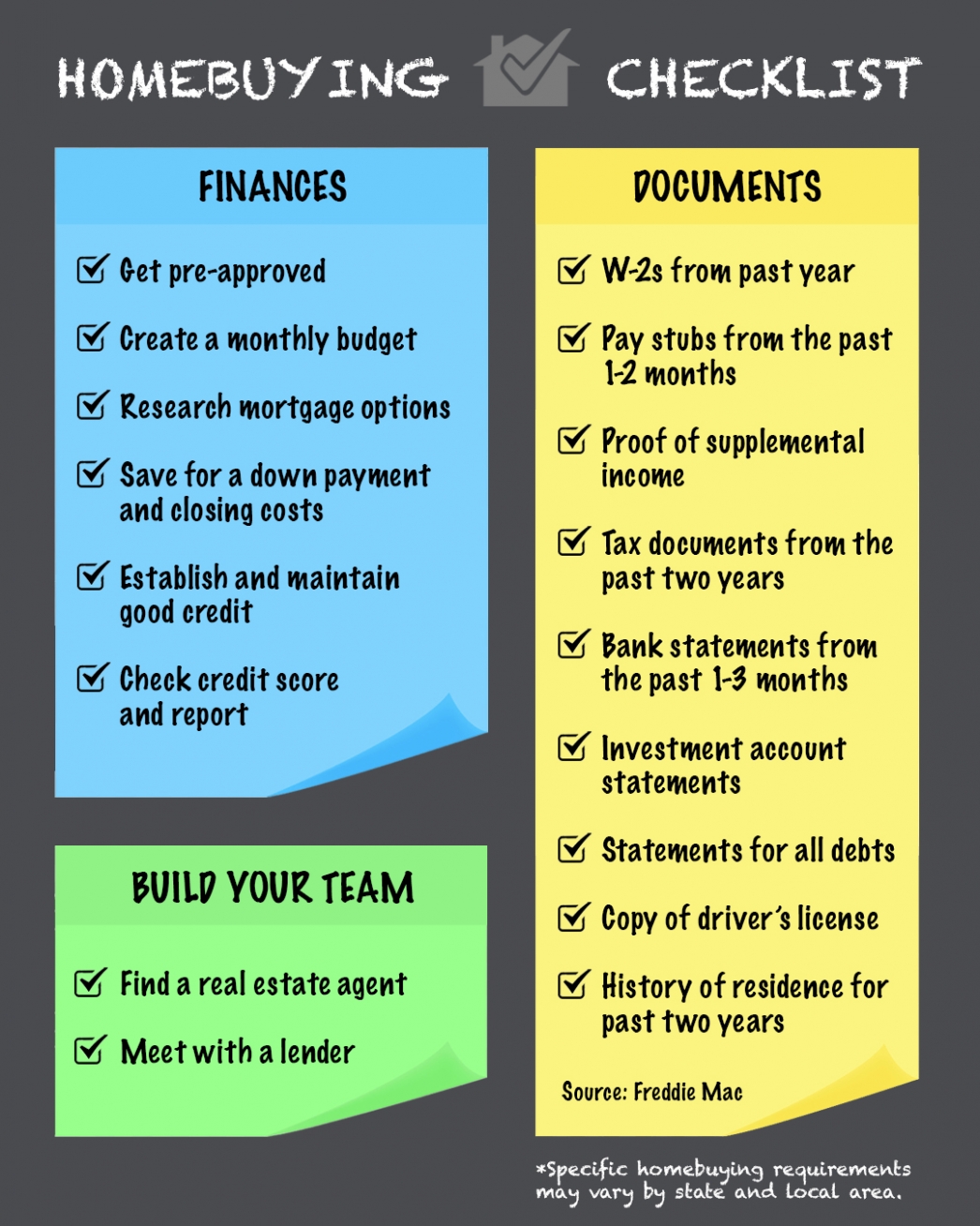

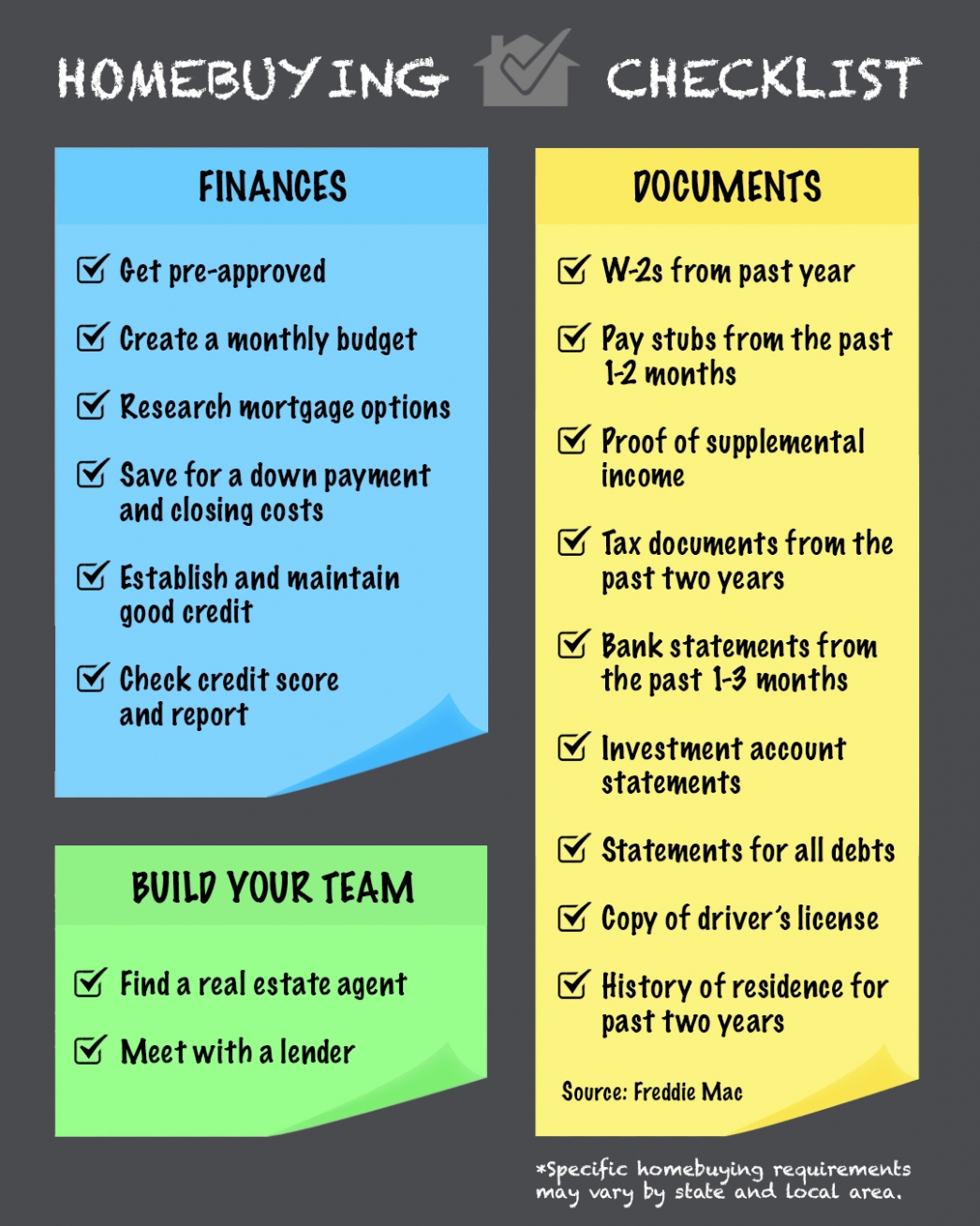

2020 Home buying Checklist

Some Highlights:

- If you’re thinking of buying a home, plan ahead and stay on the right track, starting with pre-approval.

- Being proactive about the home buying process will help set you up for success in each step.

- Make sure to work with a trusted real estate professional along the way, to help guide you through the homebuying steps specific to your area.

Things to Avoid After Applying for a Mortgage

Congratulations! You’ve found a home to buy and have applied for a mortgage! You’re undoubtedly excited about the opportunity to decorate your new home, but before you make any large purchases, move your money around, or make any big-time life changes, consult your loan officer – someone who will be able to tell you how your decisions will impact your home loan.

Below is a list of Things You Shouldn’t Do After Applying for a Mortgage. Some may seem obvious, but some may not.

1. Don’t Change Jobs or the Way You Are Paid at Your Job. Your loan officer must be able to track the source and amount of your annual income. If possible, you’ll want to avoid changing from salary to commission or becoming self-employed during this time as well.

2. Don’t Deposit Cash into Your Bank Accounts. Lenders need to source your money, and cash is not really traceable. Before you deposit any amount of cash into your accounts, discuss the proper way to document your transactions with your loan officer.

3. Don’t Make Any Large Purchases Like a New Car or Furniture for Your New Home. New debt comes with it, including new monthly obligations. New obligations create new qualifications. People with new debt have a higher debt to income ratios…higher ratios make for riskier loans…and sometimes qualified borrowers no longer qualify.

4. Don’t Co-Sign Other Loans for Anyone. When you co-sign, you are obligated. As we mentioned, with that obligation comes higher ratios as well. Even if you swear you will not be the one making the payments, your lender will have to count the payments against you.

5. Don’t Change Bank Accounts. Remember, lenders need to source and track assets. That task is significantly easier when there is consistency among your accounts. Before you even transfer any money, talk to your loan officer.

6. Don’t Apply for New Credit. It doesn’t matter whether it’s a new credit card or a new car. When you have your credit report run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), your FICO® score will be affected. Lower credit scores can determine your interest rate and maybe even your eligibility for approval.

7. Don’t Close Any Credit Accounts. Many clients erroneously believe that having less available credit makes them less risky and more likely to be approved. Wrong. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those determinants in your score.

Bottom Line

Any blip in income, assets, or credit should be reviewed and executed in a way that ensures your home loan can still be approved. The best advice is to fully disclose and discuss your plans with your loan officer before you do anything financial in nature. They are there to guide you through the process.

Buying a Home: Do You Know the Lingo? [INFOGRAPHIC]

![Buying a Home? Do You Know the Lingo? [INFOGRAPHIC] | MyKCM](https://desireestanley.com/files/2019/08/20190816-MEM.jpg)

![Buying a Home? Do You Know the Lingo? [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2019/08/13124327/20190816-MEM-1046x1354.jpg)

Some Highlights:

- Buying a home can be intimidating if you’re not familiar with the terms used throughout the process.

- To point you in the right direction, here’s a list of some of the most common language you’ll hear when buying a home.

- The best way to ensure your home-buying process is a positive one is to find a real estate professional who will guide you through every aspect of the transaction with ‘the heart of a teacher.’